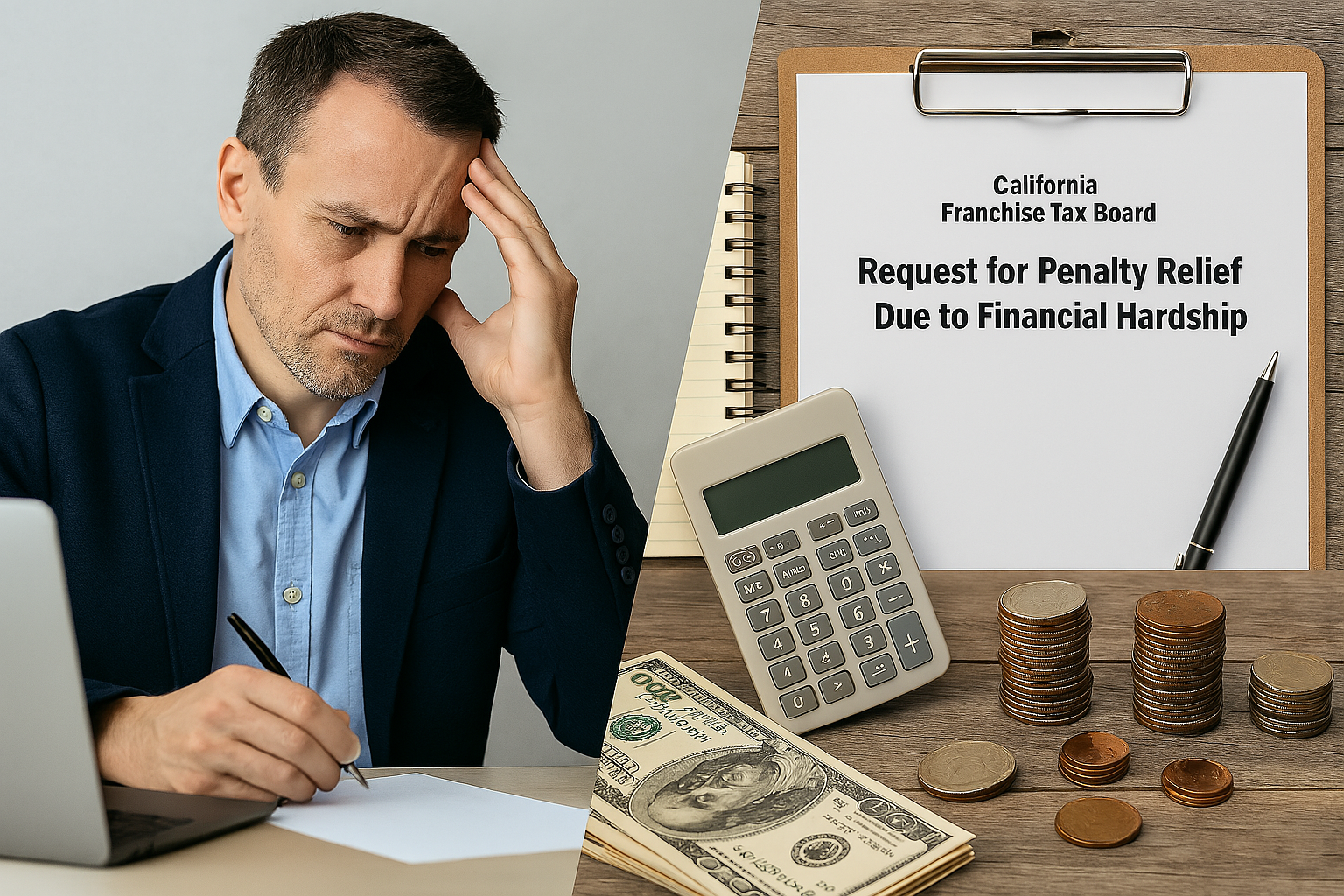

In the case of most California-based businesses, financial difficulty is not merely an issue but rather a fact, more so following any disruption such as the COVID-19 pandemic, record inflation, and supply chain crisis. The California Franchise Tax Board (FTB) will charge heavy penalties when taxes are not paid on time or payment is not made even partially.

Yet, the state provides an organized approach to seeking relief from the penalty in case your business can prove to have suffered a legitimate financial crisis. A tax law attorney is someone who can help in these situations.

This blog will discuss the ways businesses can go about this process, what constitutes a reasonable cause, as well as how to make a good argument to the FTB.

1. Understanding the Types of Penalties Businesses Face

The type of penalties that have been imposed should be identified before a request can be made to get relief. In business terms, they might involve:

- Penalties for late filing

- Penalties for late payment

- Possible penalties for estimated tax

- Accuracy-related penalties

- Underpayment penalties

All of them have different rules and thresholds, and knowing the one that will apply in your case allows you to better align your request for relief, given the circumstances.

2. What Qualifies as “Reasonable Cause” for Penalty

According to the California Revenue and Taxation Code (RTC) sections 19132 and 19133, businesses can acquire some relief on the penalty under the condition that the non-compliance reason was based on reasonable cause, but not willful neglect.

Examples that tend to apply:

- Natural hazards (e.g., wildfire, earthquakes)

- Epidemics (e.g., COVID-19)

- Disruption in the economy resulting in the collapse of the cash flow

- Insolvency or bankruptcy petitions

- Theft, embezzlement, or cyberattacks that result in the loss of information and money

Every demand should be supported by objective records that bridge the gap between suffering and non-compliance.

3. The Impact of COVID-19 and Market Downturns

In the era of COVID-19, the FTB experienced extensive financial hardship and extended several due dates for filing and paying. Those businesses that did not meet deadlines as a result of:

- Office closures

- Employee layoffs

- Loss of clients or jobs, Loss of contracts

- Revenue Losses: Drastic Revenue Losses

had an avenue to seek abatement, particularly where these conditions were extended to subsequent fiscal years.

To this day, it is possible to cite pandemic-era financial records, including loss statements or SBA loan applications, as examples of supporting reasonable cause claims. Even during an IRS payroll audit, one can ask for some time in case of critical situations.

4. Preparing and Submitting a Penalty Abatement

The businesses may apply to obtain FTB penalty reliefs through the submission of:

Form FTB 2917- Reasonable Cause -Business Entity

An elaborate written description of the chronology of the hardship, how the hardship affected the sales tax compliance, and the measures taken to address it.

Attach:

- Profit and Loss statements

- Bank records

- Insurance (in case it is possible)

- Notice of layoff file or vendor cancellation

- Letters from legal or financial counsellors

The critical issue is to demonstrate a clear, causal relationship between the suffering and the inability to observe the taxation rules.

Just keep a record of your case, be open, and consult professional help where needed. You can then have your business back on track and avoid excess tax.